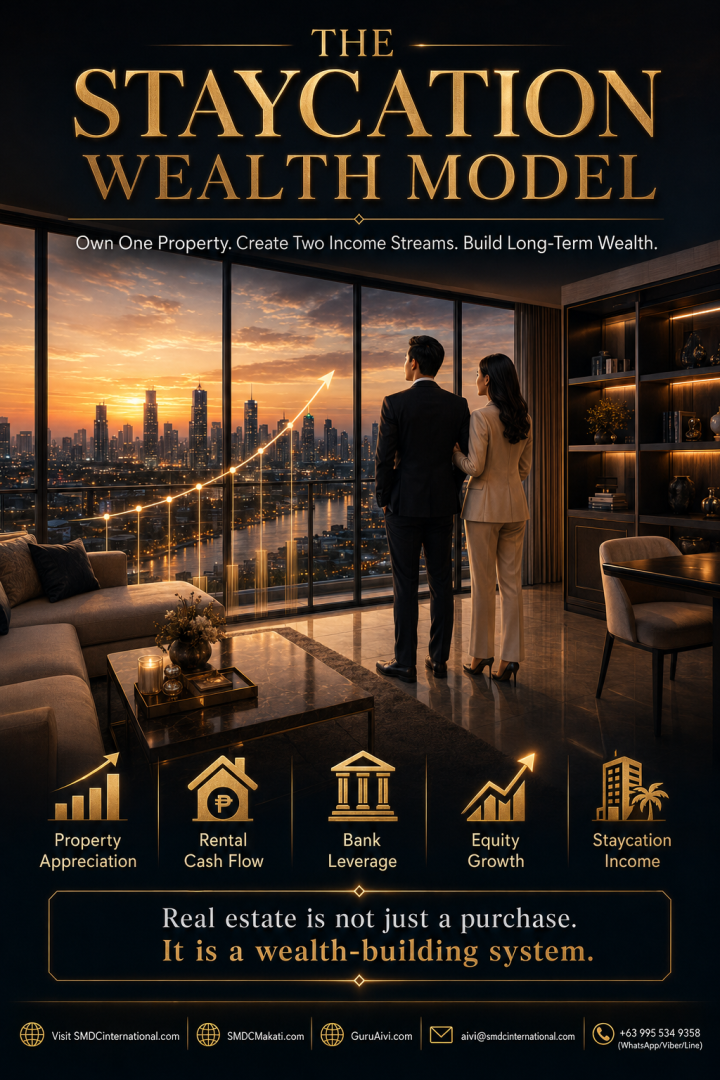

The Staycation Wealth Model: How One Property Can Create Income, Build Equity and Support Long-Term Wealth

Real estate is often described as a long-term investment, but the strongest property strategies go beyond simply buying a condominium and waiting for its value to increase.

A carefully selected property can potentially serve several purposes at the same time. It may provide a place to live, generate rental income, operate as a staycation unit, build ownership equity, benefit from long-term appreciation and eventually become the foundation of a larger property portfolio.

This is the idea behind the Staycation Wealth Model.

It is not a promise of automatic profit or guaranteed financial freedom. It is a structured approach to property ownership based on responsible financing, strong locations, realistic income projections, disciplined operations and patient portfolio growth.

One Property, Multiple Wealth-Building Functions

A condominium should not be viewed only as a physical unit. From an investment perspective, it may function as an income-producing and wealth-building asset.

A well-chosen property may create value through five primary channels:

- Property appreciation

- Long-term rental cash flow

- Staycation booking income

- Bank leverage

- Equity growth

The most important idea is that these benefits can work together.

Rental or staycation revenue may help cover financing and operating costs. Loan payments may gradually reduce the outstanding balance. As the loan balance declines, the owner’s equity may increase. At the same time, a strategically located property may appreciate in value as surrounding infrastructure, employment and demand develop.

The property therefore becomes more than a purchase. It becomes part of a broader financial system.

Why Real Estate Can Make Money Work Harder

Bank savings and real estate serve different financial purposes.

Savings accounts provide liquidity, stability and immediate access to funds. They are essential for emergencies, short-term expenses and financial security. However, ordinary savings accounts may offer relatively limited growth.

Real estate, on the other hand, is generally treated as a longer-term asset. It may provide potential appreciation, recurring income and ownership equity, but it also requires capital, management, patience and risk tolerance.

Using an illustrative ₱5,000,000 example:

- At 2% annual bank interest, ₱5,000,000 may generate approximately ₱100,000 in one year.

- At a 6% illustrative property appreciation rate, a ₱5,000,000 property may increase in value by approximately ₱300,000 in one year.

This is only a simplified comparison. A real property investment also involves financing costs, taxes, association dues, maintenance, vacancy risks, insurance and transaction expenses.

Property appreciation is also not guaranteed. Values can remain flat or decline depending on the economy, location, development quality and market conditions.

The real advantage of property is not appreciation alone. A well-managed unit may also generate rental or staycation revenue while the owner continues building equity.

A balanced investor therefore does not abandon savings. Instead, the investor maintains sufficient liquidity while gradually acquiring quality assets that may grow and produce income.

The Power of Responsible Leverage

One reason real estate has become a common wealth-building vehicle is the availability of financing.

Unlike many investments that require full payment upfront, qualified property buyers may acquire real estate through a combination of personal equity and bank financing.

Using the consistent illustrative example:

- Initial property value: ₱5,000,000

- Initial equity at 20%: ₱1,000,000

- Illustrative bank financing at 80%: ₱4,000,000

This means a qualified buyer may control a ₱5,000,000 asset without initially paying the entire value in cash.

This is called leverage.

Leverage may help an investor:

- Enter the market with less initial capital

- Preserve funds for reserves, furnishing or other investments

- Control a larger asset

- Benefit from potential appreciation on the full property value

- Build equity as financing obligations are repaid

However, leverage can magnify both opportunity and risk.

A larger loan creates larger monthly obligations. Interest rates may change. Rental income may be lower than expected. The unit may remain vacant. Repairs or association dues may increase. A property that appears affordable based only on the down payment may become difficult to sustain once all expenses are included.

Responsible leverage therefore requires:

- Stable and sufficient income

- Affordable monthly obligations

- Emergency reserves

- Realistic rental assumptions

- Insurance

- Careful review of interest rates and loan terms

- A long-term holding strategy

The strongest property investment is not necessarily the one with the highest loan amount. It is the one the investor can comfortably sustain even during vacancies, repairs or economic uncertainty.

Location Creates Long-Term Demand

A beautiful unit in a weak location may struggle to produce consistent demand. A more modest unit in a highly connected area may perform better over time.

Location affects nearly every part of a property investment:

- Rental demand

- Occupancy

- Nightly rates

- Tenant quality

- Resale potential

- Convenience

- Future appreciation

- Operating stability

Strong locations are usually connected to the places people regularly need.

These may include:

- Central business districts

- Employment centers

- Airports

- Railways and transport terminals

- Shopping malls

- Schools and universities

- Hospitals

- Tourism destinations

- Government offices

- Entertainment and lifestyle districts

Infrastructure also plays an important role.

New roads, bridges, transport lines, airports, commercial centers and business districts may improve accessibility and stimulate demand. As communities develop, more residents, workers, students, travelers and businesses may enter the area.

However, investors should distinguish between confirmed infrastructure and speculative announcements. A proposed project may be delayed, redesigned or cancelled. Investment decisions should be based on existing demand and credible development plans rather than marketing claims alone.

A strong property begins with a location that people continually need—not merely a location that looks promising on a brochure.

How Tenants Can Help Build Ownership Equity

Long-term rental is one of the most straightforward ways to generate income from a condominium.

When a tenant pays rent, the income may help cover:

- Monthly loan payments

- Association dues

- Maintenance

- Property taxes

- Insurance

- Repairs

- Property management

- Other operating costs

Using an illustrative monthly scenario:

- Gross long-term rent: ₱35,000

- Estimated monthly loan payment: ₱28,000

- Remaining amount before other expenses: ₱7,000

The ₱7,000 difference should not automatically be treated as profit.

The owner may still need to deduct:

- Association dues

- Property taxes

- Insurance

- Maintenance

- Repairs

- Vacancy allowance

- Leasing commissions

- Management fees

- Furnishing replacement

- Legal and administrative costs

Nevertheless, the tenant’s rental payment may still support the ownership process.

As monthly financing obligations are paid, part of the payment may reduce the outstanding principal. As the outstanding loan balance declines, the owner’s equity may increase.

Owner’s equity can be understood as:

Current property value minus outstanding loan balance

For example, if a property is worth ₱5,500,000 and the remaining loan is ₱3,500,000, the owner may have approximately ₱2,000,000 in equity before taxes, selling costs and other obligations.

This is why rental income can be powerful. Even when monthly net cash flow is modest, the investor may still be building ownership through principal repayment and potential appreciation.

Staycation or Long-Term Rental?

A property investor must decide how the unit will be operated.

The two most common strategies are long-term rental and short-term staycation operations.

Long-Term Rental

A long-term tenant usually signs a lease for several months or one year.

Potential advantages include:

- More predictable monthly rent

- Fewer guest turnovers

- Simpler operations

- Lower cleaning frequency

- Reduced platform dependence

- Less daily management

- More stable occupancy

Potential disadvantages include:

- Lower gross revenue potential

- Limited ability to adjust rates during high-demand periods

- Longer exposure to one tenant

- Possible collection or eviction challenges

- Reduced flexibility for owner use

Staycation Operations

A staycation unit is rented to guests on a nightly or short-term basis.

Potential advantages include:

- Flexible nightly pricing

- Higher gross revenue potential

- Ability to benefit from weekends, holidays and events

- More flexibility for personal use

- Access to business travelers, tourists and local guests

Potential disadvantages include:

- More active management

- Frequent cleaning and turnover

- Platform fees

- Guest complaints and reviews

- Seasonal occupancy

- Higher wear and tear

- Building or condominium restrictions

- Licensing and tax obligations

Using an illustrative ₱5,000,000 property:

Long-Term Rental Example

Gross monthly rent: approximately ₱35,000

Staycation Example

- Average daily rate: ₱3,500

- Occupancy: approximately 70%

- Booked nights: approximately 21 nights

- Gross monthly booking revenue: approximately ₱73,500 before expenses

The staycation figure appears significantly higher, but it is gross revenue—not net profit.

Staycation operations may involve additional cleaning, utilities, platform charges, supplies, management, marketing, taxes, repairs and vacancy risk.

The best strategy depends on:

- Location

- Building rules

- Guest demand

- Tenant demand

- Management capacity

- Personal availability

- Operating costs

- Investment objectives

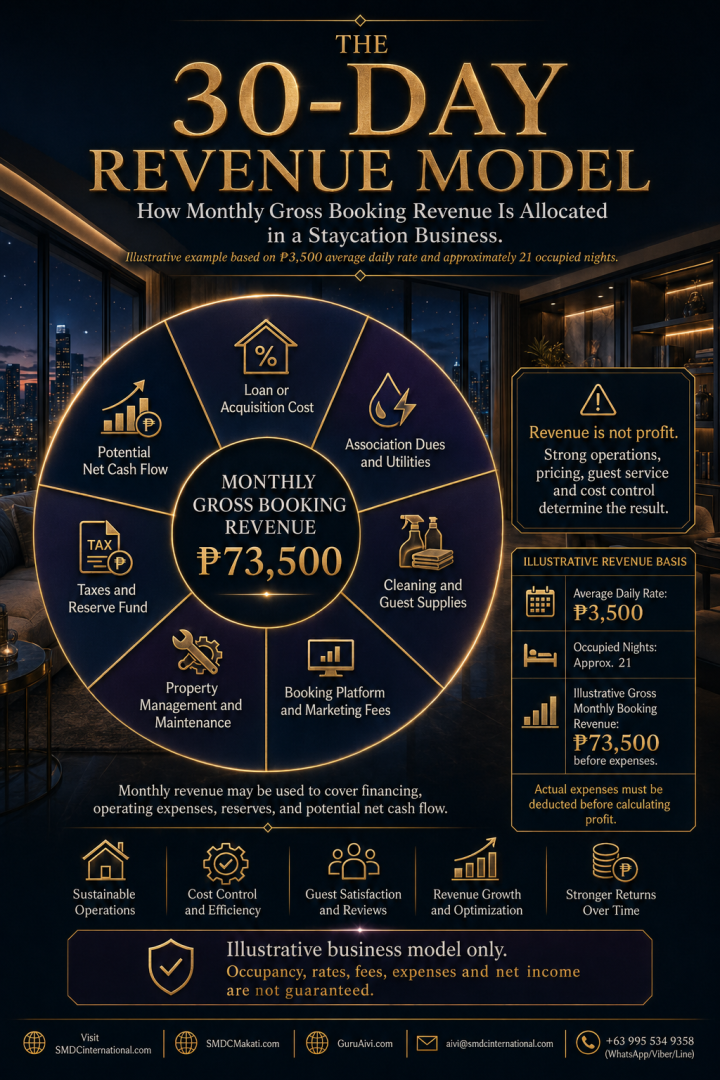

Understanding the 30-Day Staycation Revenue Model

The most common mistake in evaluating a staycation property is confusing gross revenue with profit.

Gross booking revenue is the total amount collected from guests before expenses.

Using the illustrative example:

- Average daily rate: ₱3,500

- Occupied nights: approximately 21

- Gross monthly booking revenue: approximately ₱73,500

That revenue must then be allocated across several categories.

1. Loan or Acquisition Cost

The property may have a monthly bank amortization or developer payment obligation.

This is often the largest recurring expense.

2. Association Dues and Utilities

These may include:

- Condominium association dues

- Electricity

- Water

- Internet

- Cable or streaming services

- Parking charges

- Building access fees

Staycation units typically consume more utilities than vacant investment units.

3. Cleaning and Guest Supplies

Every guest turnover may require:

- Cleaning services

- Laundry

- Toiletries

- Drinking water

- Tissue products

- Coffee and refreshments

- Replacement towels and linens

- Basic maintenance materials

4. Booking Platform and Marketing Fees

Online booking platforms may deduct service charges or commissions.

The owner may also spend on:

- Social media promotion

- Photography

- Advertising

- Discounts

- Affiliate commissions

- Direct-booking systems

5. Property Management and Maintenance

Owners who cannot personally operate the property may hire a manager.

Property management can include:

- Guest communication

- Check-in and check-out

- Cleaning coordination

- Pricing management

- Maintenance

- Complaint handling

- Review management

- Revenue tracking

6. Taxes and Reserve Fund

Taxes may apply depending on the business structure and applicable regulations.

A reserve fund should also be maintained for:

- Repairs

- Appliance replacement

- Furniture replacement

- Air-conditioning maintenance

- Emergency expenses

- Unplanned vacancies

- Major renovations

7. Potential Net Cash Flow

Only after all expenses are deducted can the investor estimate true net cash flow.

A property generating ₱73,500 in gross bookings may produce significantly less net income after expenses. In some months, there may be no profit at all.

This does not automatically make the investment unsuccessful. Part of the revenue may still be supporting loan repayment and equity growth. However, the owner must understand the difference between income, cash flow and equity.

From One Property to a Portfolio

A successful first property may eventually become the foundation of a larger real estate portfolio.

But scaling should never be automatic.

Investors should not acquire a second property simply because the first property has increased in value or because another financing offer becomes available.

A portfolio should grow only when the first investment demonstrates financial stability.

Before acquiring another property, review:

- Actual monthly net cash flow

- Occupancy history

- Maintenance costs

- Loan performance

- Emergency reserves

- Debt-to-income ratio

- Financing capacity

- Market demand

- Insurance coverage

- Personal income stability

A possible portfolio progression may look like this:

First Property: Smart Beginning

The first property teaches the investor how to finance, operate, maintain and evaluate real estate.

Second Property: Additional Income Stream

A second unit may diversify income, but it also doubles management responsibilities and financial obligations.

Third Property: Portfolio Diversification

The investor may acquire a unit in another location or market segment to reduce dependence on one property.

Fourth Property: Wealth Acceleration

A larger portfolio may generate stronger combined cash flow and equity, but risk also increases.

Fifth Property: Greater Financial Flexibility

A mature portfolio may provide several income streams and more strategic choices, provided the assets remain sustainable.

Four principles support responsible portfolio growth:

- Property appreciation

- Accumulated equity

- Reinvested cash flow

- Strategic financing

However, the investor should never rely exclusively on appreciation or future refinancing. Cash flow, reserves and affordability must remain the foundation.

The Real Estate Investment Journey

Property investing should be approached as a process rather than a single purchase.

A practical seven-stage roadmap may include the following:

Stage 1: Identify the Right Property

Study:

- Location

- Developer reputation

- Project quality

- Accessibility

- Rental demand

- Competing properties

- Building policies

- Long-term development potential

Do not choose based only on appearance, discounts or emotional pressure.

Stage 2: Review Financing and Affordability

Understand:

- Required initial equity

- Monthly payment

- Interest rates

- Loan duration

- Insurance

- Taxes

- Closing costs

- Association dues

- Furnishing budget

- Emergency reserves

The investment should remain manageable even if income is lower than expected.

Stage 3: Acquire with a Clear Strategy

Decide the intended use before buying.

Will the property be:

- Owner-occupied?

- Used for long-term rental?

- Operated as a staycation?

- Held for resale?

- Used as part of a family estate?

- Combined with personal and rental use?

A clear strategy prevents expensive changes later.

Stage 4: Prepare the Unit

A rental or staycation unit must be designed for the target market.

Preparation may include:

- Furniture

- Appliances

- Lighting

- Storage

- Internet

- Bedding

- Security

- Photography

- Listing creation

- House rules

- Guest or tenant documentation

Stage 5: Operate and Monitor Cash Flow

Track the property monthly.

Monitor:

- Revenue

- Occupancy

- Daily rates

- Rental payments

- Loan payments

- Utilities

- Cleaning

- Repairs

- Platform fees

- Taxes

- Reserve funds

- Net cash flow

What is not measured cannot be managed properly.

Stage 6: Build Equity and Evaluate the Next Opportunity

After establishing performance, review whether the property is meeting its goals.

Do not expand based on projections alone. Use actual operating results.

Stage 7: Create a Sustainable Portfolio and Legacy

A portfolio should eventually support—not weaken—the investor’s quality of life.

The ultimate goal may be:

- Additional income

- Retirement support

- Family security

- Business diversification

- Generational wealth

- Greater financial flexibility

Build Wealth Without Sacrificing Financial Stability

Real estate should support the life the investor is building—not place it at unnecessary risk.

A property may contribute to:

- Passive income potential

- Long-term appreciation

- Time flexibility

- Portfolio growth

- Family legacy

But these outcomes require patience.

A healthy property strategy does not depend on aggressive borrowing, unrealistic occupancy or constant price increases.

Instead, it follows a disciplined cycle:

- Find the right property

- Acquire responsibly

- Operate strategically

- Earn income and build equity

- Repeat only when financially ready

Financial freedom does not mean avoiding responsibility. It means creating enough stability, income and ownership that the investor has more meaningful choices.

These choices may include:

- Spending more time with family

- Reducing dependence on employment income

- Starting a business

- Traveling

- Preparing for retirement

- Supporting children

- Building a long-term family estate

The property is therefore not the final goal.

The goal is the freedom, security and opportunity the asset may help create.

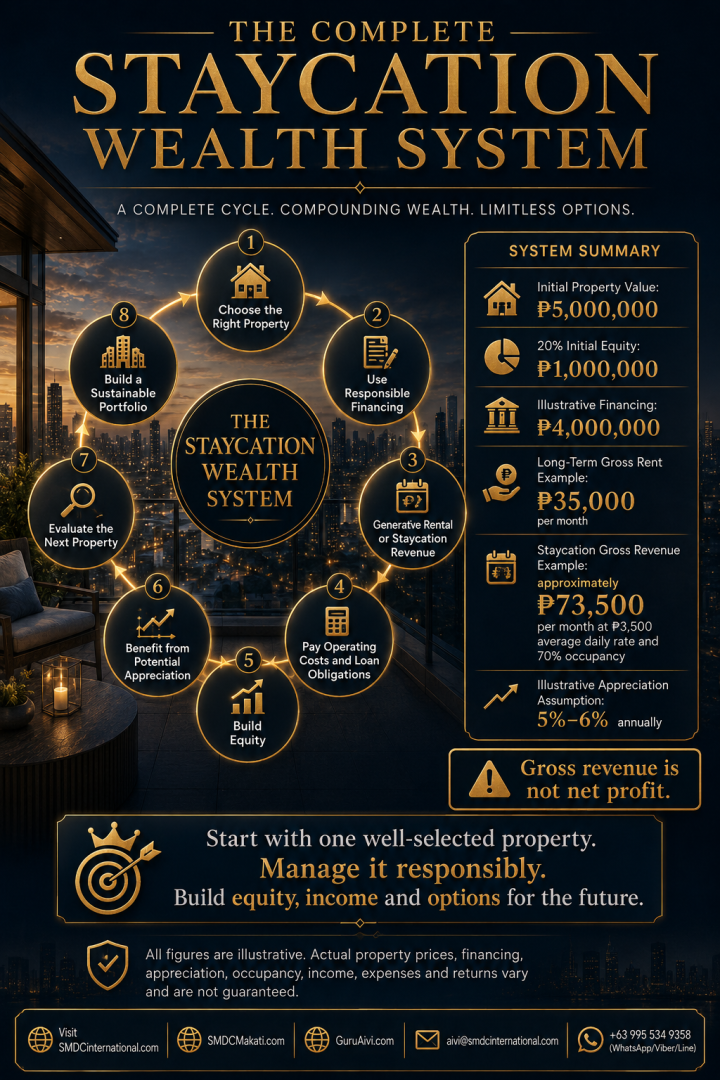

The Complete Staycation Wealth System

The entire model can be summarized as one connected cycle.

Step 1: Choose the Right Property

Begin with a strong location, credible development and realistic demand.

Step 2: Use Responsible Financing

Acquire within your means and maintain adequate reserves.

Step 3: Generate Rental or Staycation Revenue

Select the operating model that fits the location and your management capability.

Step 4: Pay Operating Costs and Loan Obligations

Treat the property as a business. Track all expenses.

Step 5: Build Equity

As the loan balance declines, ownership may increase.

Step 6: Benefit from Potential Appreciation

A strong location may increase in value over time, although appreciation is never guaranteed.

Step 7: Evaluate the Next Property

Use actual results—not optimism—to decide whether expansion is appropriate.

Step 8: Build a Sustainable Portfolio

Grow gradually while protecting cash flow, reserves and financial stability.

Using the consistent illustrative example:

- Initial property value: ₱5,000,000

- 20% initial equity: ₱1,000,000

- Illustrative financing: ₱4,000,000

- Long-term gross rent example: ₱35,000 per month

- Staycation gross revenue example: approximately ₱73,500 per month before expenses

- Illustrative appreciation assumption: 5%–6% annually

These figures are not promises. They are educational assumptions intended to demonstrate how a property investment may be structured.

Actual outcomes will depend on:

- Property price

- Interest rates

- Loan approval

- Rental demand

- Staycation restrictions

- Occupancy

- Daily rates

- Operating costs

- Taxes

- Maintenance

- Market performance

- Management quality

Final Perspective: Start with One Strong Property

The Staycation Wealth Model is not about buying as many units as possible.

It is about starting with one well-selected property and managing it intelligently.

A strong investment process should include:

- Careful location analysis

- Responsible financing

- Realistic revenue estimates

- Accurate expense tracking

- Professional property management

- Adequate emergency reserves

- Compliance with building and government regulations

- Patient equity growth

- Disciplined portfolio expansion

The right property may generate income, build ownership and increase in value.

The wrong property—or the right property purchased with the wrong financing—may create financial pressure.

The difference is strategy.

Start with one well-selected property. Manage it responsibly. Build equity, income and options for the future.

Begin Your SMDC Real Estate Investment Journey

Explore SMDC property options for personal use, long-term rental, investment and potential staycation operations.

Visit:

SMDCinternational.com

SMDCMakati.com

GuruAivi.com

Email:

WhatsApp, Viber or Line:

+63 995 534 9358

Disclaimer: This article is for general educational and marketing purposes only. All figures are illustrative. Property prices, financing approval, interest rates, appreciation, occupancy, income, expenses, taxes and returns vary and are not guaranteed. Buyers should review their financial capacity, loan terms, project rules, rental and staycation regulations, taxes, insurance and operating costs before making an investment decision.